Closing Costs On The Rise In Mass., U.S. | Distressed sales equal higher fees for buyers

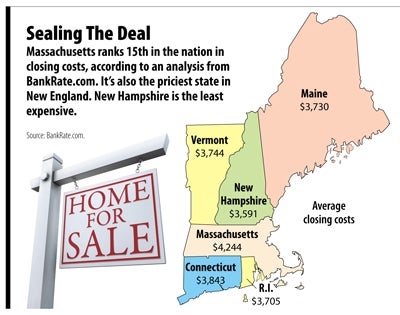

Massachusetts is the 15th costliest state in the nation when it comes to closing costs for buying a home, according to a report by Bankrate.com, a national financial advice website.

Last year the average cost to close on a $200,000 mortgage with a 20-percent down payment in Massachusetts was $4,025. This year, that figure was $4,244, including $1,594 for loan origination and $2,650 for title and closing fees.

And the prices are rising. In Massachusetts, total closing costs rose more than 5.4 percent. Nationally, the increase was 8.8 percent.

What’s driving the increases here and around the United States? There are several different factors, but one important one is the number of foreclosured homes that remain on the market.

Today there are more distressed properties being bought and sold. And distressed properties come with a lot of legal paperwork, noted Nicole Reeves Lavallee, an independent Worcester-based real estate lawyer. And more legal work means higher legal fees.

“If you’re talking about a short-sale property, you can easily look at a good 30 hours to get the paperwork done,” she said. “With that much time and work, you have to charge more. You’re doing an exorbitant amount of work.”

Not Just Attorneys

But it’s not just attorneys’ fees that are driving up the prices.

Overall, there’s just more due diligence completed by all parties involved in a real estate transaction, according to Greg McBride, senior financial analyst with Bankrate.com

“After everything we’ve been through in the housing market, everyone is a little more cautious today, and more scrutiny can lead to higher costs,” he said.

That means not only are attorneys’ costs going up, but so are appraisal costs, title insurance and the dozen or so other fees that come along with purchasing a home.

Most of the increases are being recorded from third parties involved in the closing, not from the lenders themselves, pointed out Jon Skarin, director of legislative and regulatory policy for the Massachusetts Bankers Association. Third parties include appraisers, attorneys and insurance agents.

“A lot of these costs aren’t necessarily under the control of the bank,” he said.

Jeff Bajema, senior vice president of retail lending at UniBank in Whitinsville, agreed that appraisers and attorneys are taking extra due diligence given the realities of the market.

But “our costs haven’t changed,” he added.

The increased fees by appraisers and attorneys are not a money grab, officials said. More work requires more resources, which costs more money.

Michael O’Hara, a 25-year veteran appraiser in Worcester with O’Hara-Buthray Associates, said he hasn’t seen appraisal fees increase — yet.

“In this market, I haven’t seen anyone raise fees,” he said. But, he added, price increases could be coming soon.

Starting in September, appraisers will be operating under new federal regulations that require home mortgages sold on the secondary market to organizations like Fannie Mae and Freddie Mac to be appraised with a new, more detailed form known as the Uniform Appraisal Dataset (UAD).

O’Hara said his firm has just begun using the UAD so he’s unsure what the impact will be on costs. But he did say the form is longer and much more labor intensive than the current process.

Bankrate.com also pointed out that the survey could have some wrinkles.

The website uses estimates from lenders to calculate the closing costs. There could be a difference between an estimate and the actual charges, McBride said. Some lenders may be slightly overestimating closing costs because new federal regulations require the estimates to be within a certain percentage of the actual costs.

WBJ Web Partners

Most Recent

Most Recent

0 Comments