Savings, for whom? More employers find advantages in health savings accounts

It’s either the future of health care or a potential source of financial problems, a means of controlling soaring medical costs or a way to leave middle-class Americans footing the bill.

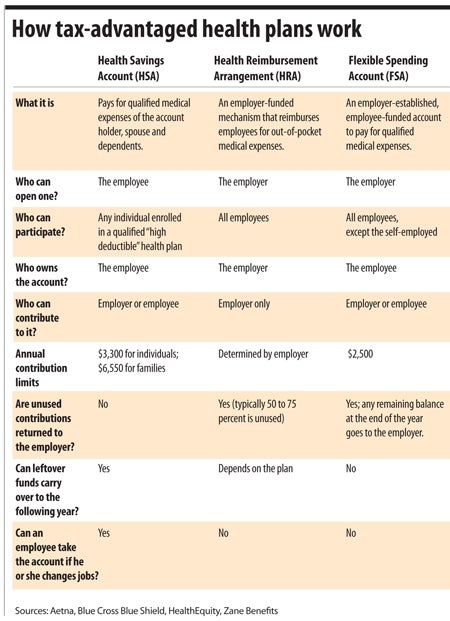

Welcome to the debate over health savings accounts (HSAs), a lower-premium, higher-deductible health insurance plan that relies on an employee-maintained, tax-free savings account to pay for most medical expenses.

That’s music to most employers’ ears, with the number of firms nationwide offering HSAs increasing from 7 percent in 2007 to 17 percent today, according to the Kaiser Family Foundation.

Local companies have been looking to cash in on this trend. Hudson-based Avidia Bank has been actively marketing HSAs to individuals for the past two years, attracting some $4 million in deposits over that time, according to Robert Conery,

Avidia’s executive vice president and chief operating officer.

In December, the bank began selling HSA plans to the much larger employer and benefit administrator markets, Conery said. As a result, HSAs are expected to jump from representing 0.4 percent of Avidia’s deposit base today to 8 percent by 2019.

But Avidia expects most of its new customers to come from other parts of the country over the next few years, Conery said. In Massachusetts — where low- or no-deductible plans from health maintenance organizations (HMO) dominate the landscape — HSAs have received a tepid response.

Just 2.8 percent of Bay State residents are enrolled in an HSA, well below the 7 percent average nationwide, according to America’s Health Insurance Plans (AHIP), a health insurance trade group. Only six states have smaller percentages of their residents enrolled in HSAs.

But things are starting to change slowly in the commonwealth.

The number of Bay State residents covered under HSAs has tripled, from 50,000 in 2008 to more than 150,000 today, according to AHIP. And many companies with less than 50 employees will select their 2014-15 health insurance offerings in April, said Chris Powers, senior vice president of Benefit Development Group in Worcester, so that figure could grow.

And an Associated Industries of Massachusetts (AIM) survey found that the number of Bay State companies offering HSAs grew from 8 percent in 2012 to 10 percent in 2013.

“It’s growing, and it will continue to grow,” said David Przesiek, vice president of sales at Fallon Community Health Plan in Worcester.

What do employers like about HSAs?

First, total annual premiums are about $1,000 lower per individual and $2,500 per family than those of a traditional health plan, according to Kaiser. So, firms spend about $700 less a year for each individual and about $925 less for each family enrolled in an HSA.

And HSAs are expected to generate greater savings for employers in the long run as workers modify their behavior in response to having to pay for more of their medical expenses.

“Now the employee has skin in the game,” Conery said. “Health care is not an entitlement anymore.”

Aside from a fully covered annual physical, people with an HSA are responsible for every dollar of their medical bills — including prescription drugs — until they hit their deductible, which, in Massachusetts, is at least $1,250 for individuals and $2,500 for families (and often much higher).

Therefore, HSA proponents expect the size and frequency of claims filed will fall as enrollees adopt healthier lifestyles and price shop when they need prescriptions or medical procedures. That should result in lower company premiums in subsequent years, said Russ Sullivan, AIM’s vice president for health care solutions.

The tax status of HSAs presents more savings opportunities for companies, Conery said. Worker contributions are made on a pre-tax basis, which lowers employers’ payroll taxes, he said. And employer contributions don’t count against the payroll tax.

The 2018 implementation of the “Cadillac Tax” on employers that offer only plans with high premiums and no deductibles should also hasten the spread of low-cost alternatives like the HSA, said Todd Berkley, president of Minnesota-based HSA Consulting Services.

But HSAs represent a drastic change from the status quo in Massachusetts and are often seen by workers and companies alike as too risky. Universities, hospitals, and union-based workforces represent many of the Bay State’s leading employers, and all of those sectors have traditionally been aligned with benefit-rich plans like the HMO, Berkley said.

Shifting from HMOs?

Companies often introduce HSAs as a step down from an already existing high-deductible plan when they’re faced with major premium increases each year, Powers said. But many Massachusetts employers are just now moving from HMO plans to ones with higher deductibles, meaning the proliferation of HSAs locally is likely several years away, he said.

People opting for an HSA on the federally-run Affordable Care Act exchanges spend, on average, $87.76 — or 11 percent — less on premiums each month than those who opt for traditional health coverage, an HSA Consulting Services study found.

But HSAs in Massachusetts have, on average, a much lower deductible than in other states, limiting the cost savings, said Eric Remjeske, president and co-founder of Devenir, a Minneapolis-based HSA consulting firm.

Philosophical disagreements also prompt Massachusetts underwriters to price HSAs less aggressively than in other states, Remjeske said.

Many Bay State employers find the HSA plan design troublesome, prompting far fewer to offer it to their workers. For example, some companies object to the lack of coverage for prescription drugs, said Bill Randell, principal and co-founder of Advantage Benefits in Worcester. “That seems to be the dealbreaker,” he said.

Others find it problematic that their workers could be on the hook for several thousand dollars in hospital expenses — such as for childbirth — without support from the insurance company.

“Employers become very concerned about the expenses their employees might have,” Powers said.

Yet, 11 percent of workers nationwide who are offered HSAs opt for such a plan, Kaiser found. That’s up from 6 percent in 2010.

Both Fallon and Reliant Medical Group have been offering an HSA option for the past half-decade to their own employees, with both Worcester-based organizations contributing at least $500 annually to each worker’s plan.

Roughly 750 of Fallon’s 1,100 employees are enrolled in an HSA, according to Falllon’s Przesiek. At Reliant, just 17 out of 1,700 employees are enrolled, said Karen Martucci, the company’s director of compensation and benefits.

“It’s a very small group (of enrollees),” Martucci said, “but we feel it’s worth keeping.”

WBJ Web Partners

Most Recent

Most Recent

0 Comments