Health insurers, business battle feds over risk-rating factors

Fallon Health and other smaller Massachusetts-based health insurers have been raising objections and concerns about a provision in the federal Affordable Care Act (ACA) that imposes multi-million-dollar risk assessments on them to be paid to bigger providers.

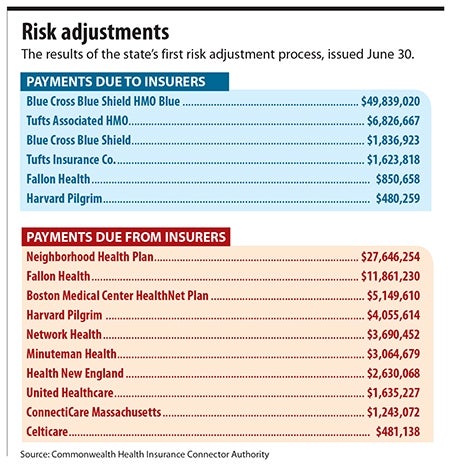

Paymets under those assessments are due by the end of this month.

Insurers across the country are now submitting proposed 2016 premiums to their state regulators for approval on federal exchanges. Until final premium adjustments are approved by the Massachusetts Division of Insurance, the jury is still out on how the risk-assessment formulas will affect the ability of the smaller plans to offer lower-cost health plan options to small businesses. (The 2016 plan coverage year for Massachusetts’ small-business group plans runs from Oct. 1, 2015 through Sept. 30, 2016.)

The risk-assessment payments for some plans, including Fallon, represent a significant portion of their overall annual premiums. Fallon must dedicate 90 percent of its premium revenue to medical services and activities for patient care.

Louis Gutierrez, executive director of the Commonwealth Health Insurance Connector Authority, says there’s nothing the state can do at this point to appeal for a change to the landmark health care reform law. With payers now filing for 2016, “there’s nothing we can confidently state as an alternative at this point,” he said.

Since at least 2013, business organizations and Massachusetts officials have asked the Obama administration to approve its state-specific methodology to assess insurance risk and predict costs rather than adopt the more-general ACA guidelines that cover all states. The risk assessment model is meant to level the cost of providing health care to high-risk or newly-insured, high utilizers of care. Plans with lower-risk insureds must pay into the pool, while those that carry higher-risk patients receive payments. In Massachusetts, this skews the payment pattern in favor of larger plans with higher numbers of insureds and, therefore, more high-cost patients.

Massachusetts, which uses 11 risk-rating factors that, together, make finer distinctions than do the four ACA factors, has had nearly-universal insurance coverage since 2006, covering 96 percent of the state’s population. The state is also unique in that it has merged its individual and small-group markets to provide a break on premiums to individual subscribers. That, advocates argue, means more state-specific data are needed.

Business groups add weight

In May, the Massachusetts business community weighed in. The Associated Industries of Massachusetts (AIM), the Small Business Service Bureau, the Massachusetts Association of Health Plans, the Massachusetts Association of Health Underwriters, the Retailers Association of Massachusetts, six chambers of commerce, and Health Services Administrators, a benefits marketplace for small businesses, individuals and chambers of commerce in New England, teamed up to write to Sylvia Matthews Burwell, secretary of Health and Human Services. They advocated for Massachusetts’ unique status as the first to implement a state-based health reform law that has already insured most of its residents — and to call attention to the formation of the merged market.

But no dice. The Patrick administration had received a three-year extension, during which the state could transition from its own rating factors to the ACA’s, and last month, the Baker administration successfully extended that by a year, giving Massachusetts until Jan. 1, 2018 to become fully ACA-compliant.

Then, on June 30, the first bill came. The Health Connector issued final risk-adjustment results to the 16 health insurance carriers that serve Massachusetts’ merged market.

Flatter playing field?

Meanwhile, Health Care for All (HCFA), a consumer-oriented health advocacy group, thinks the ACA’s risk-assessment structure will be effective to “level the playing field” between plans with higher risk patients and those without. Suzanne Curry, senior health policy manager for HCFA, said it should serve to decrease costs for patients who need services the most. However, she said HCFA cannot address how health plans will react to the imposition of risk assessments. “We can’t address individual plans, but we think the system is fair,” she said, adding, “the implementation is critical.”

The ACA requires all applicants in the same age group to pay the same premium rate, and it caps premiums for the oldest age bracket at three times the rate of the premium for the youngest age bracket. Insurers, however, have no control over the number of enrollees who sign up.

Already this year, Fallon announced it will discontinue a program offered to disabled people age 21 to 64 due to economic unsustainability. That program largely does not affect the small-business community. But the fact that it attracted only 5,400 members, far below the 8,000 to 10,000 that had been anticipated, shows the make-or-break nature of enrollment numbers for smaller plans.

Additionally, new drugs, while highly effective, are also expensive, which increases costs for insurers. One notable example is Sovaldi, a Hepatitis C treatment manufactured by Gilead Sciences Inc., which costs $1,000 per pill, or $84,000 for a 12-week course.

Fallon: Risk assessment a disincentive

David Przesiek, chief sales officer for Fallon, says the ACA risk assessment serves as a disincentive for insurers to offer health and wellness programs, which have been a primary focus for Fallon since its inception in 1977. The plan has passed its savings back to individuals and small-business owners, he noted. “It’s not sitting in our savings account.”

In a recent opinion piece in the Boston Business Journal, Fallon President and CEO Patrick Hughes and his counterpart at Health New England, Maura McCaffrey, wrote that the imposition of the ACA risk adjustment on Massachusetts “grossly undervalues the cost of caring for healthy people and overestimates the cost of managing sick members… .” They warned that the result could be the termination of lower-cost insurance plans designed to attract healthier people and small business — “the people health plans would now be penalized financially for having.”

Przesiek noted that the costs have to be passed on to the small-business owner and could result in fewer choices when plans are discontinued.

“If there’s a theme here, there’s choice. [The ACA] was not meant to limit competition. In Massachusetts, it’s a law meant to solve a problem that did not exist in this commonwealth,” Przesiek says, noting that there are safeguards in the insurance system such as reinsurance (a stop-loss financial instrument), and risk corridors, which track utilization by high-cost patients, shielding insurers from unexpectedly high costs.

Fallon has submitted its rate request information to the state for 2016 and expects to hear back by Labor Day. “We are committed to small business and individuals. We will do all we can to come through on that,” Przesiek said.

WBJ Web Partners

Most Recent

Most Recent

0 Comments